8 min read

Where’s the money, Lebowski?

Hello! Recently, I opened up about launching my pet project and I got a ton of amazing comments, so I thought I’d give you the lowdown on how I budget with my app and why it’s actually worth doing.

Of course, the question of why this is even necessary is one of the most popular. There are many things that are not needed by everyone. Keeping a personal budget is one of them.

It’s cool if you don’t have to worry about finances — it’s totally normal if you don’t need to go into detail when it comes to budgeting and financial planning. But if you do need that, then my article will definitely be useful to you. I’ll explain how you can not just track your transactions, but actually plan your expenses based on your lifestyle and any other needs or wants that come up.

With more money comes higher costs

Rewording an old proverb, it’s clear why it’s important to keep a budget and track your spending. We all want to upgrade our lifestyle — eat better, take care of our health, do other cool stuff — and that often leads to increased expenses. But sometimes we make irrational purchases too, making it hard to save money. Sound familiar? We’ve all been there, thinking, “How did I manage on such a tiny salary before?”.

At the same time, many necessary expenses can suddenly move from the zone of covering your needs to the zone of luxury or showiness.

In general, I’m all too familiar with these hurdles — I’ve been there! So I figured it was time to get a budget in order.

The main trigger for me to develop my own application was the lack of a convenient tool among the existing ones on the market. I’m not saying that my application and approach are unique and universal, but maybe they will help you start budgeting or improve your current method. Next, I will tell you about the main points of budgeting and share what I lacked in other applications.

Budgeting it up

The first thing I lacked the most was budget planning. In all the apps I have seen, it was completely absent. Usually, you just indicate how much money is currently available. That’s it.

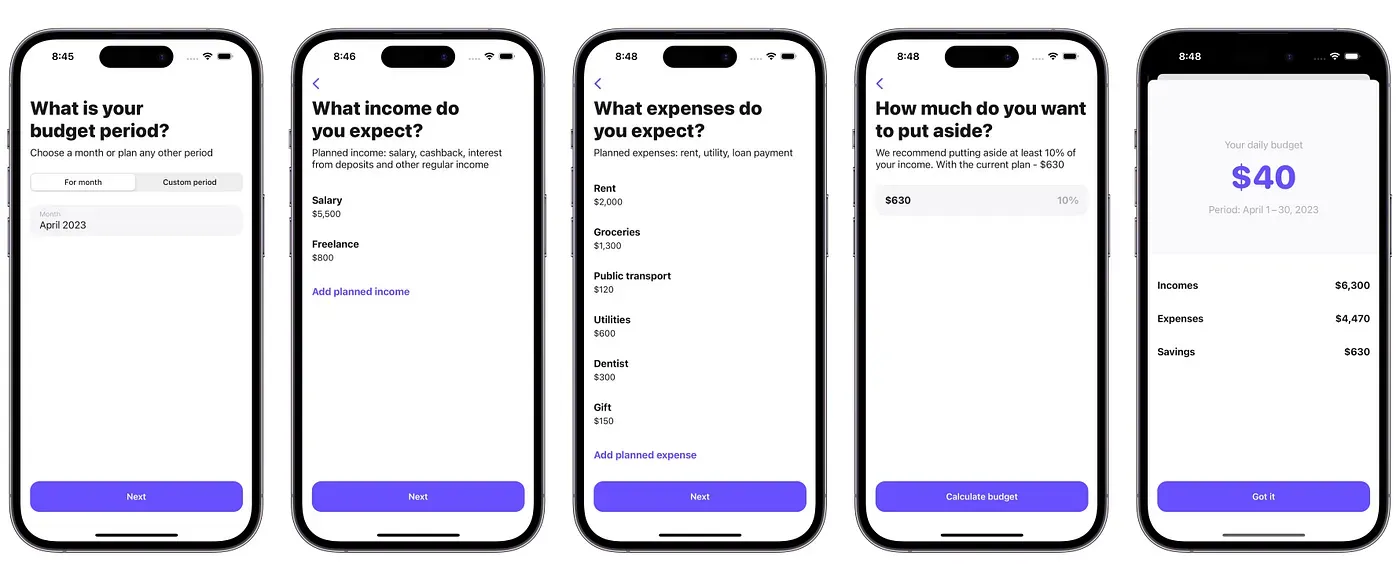

In my approach, we start with this (and will do so for each new period) — creating and planning a budget. That’s the trick: the budget in my app is not a vague concept, it has temporal boundaries. Like your monthly or quarterly budget at work. You can choose any period — a calendar month or your own. Many people find it convenient to base it on their salary date.

Next, we list income. This includes both regular payments and any sums that you are certain to expect during this period. Usually this is salary, freelance, gifts and so on.

Next, we specify regular expenses. That is, the money you already have planned to spend in this period. Rent, utilities, transport, various payments — all this falls into the category of expenses.

The last step is to specify the amount that we plan to save. This can be money for creating a financial cushion or an amount for a planned purchase in the future.

The outcome of all the planning is to get the daily budget amount. It’s simple arithmetic: subtract your expenses and savings from your income total. The remaining amount is then divided by the number of days in that budget (period).

I’ll show you the example with numbers:

- Budget: April 2023 (30 days)

- Income: Salary = $5500, Freelance project = $800, Total = $6300.

- Expenses: Rent = $2000, Groceries = $1300, Public transport = $120, Utilities = $600, Dentist = $300, Gift for a friend = $150. Total: $4470.

- Savings: I want to save $630 (10% is a good indicator).

- Free money: $6300 — $4470 — $630 = $1200.

- We divide by 30 days and get a daily budget of $40.

All amounts can be changed after creation. If you have a fluctuating income or expense, you can specify average values. The daily budget shows how much money you can spend each day without taking into account already planned operations, because these funds are already frozen and were not taken into account in the calculation.

Budget it out

As with all financial trackers, we enter operations as they appear. In my application, this needs to be done manually. Therefore, the most regular recommendation I come across is to add bank synchronization. Of course, this is convenient, but there are a few important points.

Less value. Cashless payments already depreciate money. It’s very easy to spend it. When you automatically download transactions to the app and look through them in the banking app, you don’t feel this spending either. When entering an operation manually, you give it value and get time to realize it. It’s sometimes hard for me to enter expenses into the app, but in the end I feel more aware of the money I earn and spend

Safety. As far as I know, no bank officially allows you to connect to it and access data about transactions. How this is implemented in other apps raises questions. Maybe it’s just my prejudice, but if you know any legal and safe ways — please share, I will be very grateful.

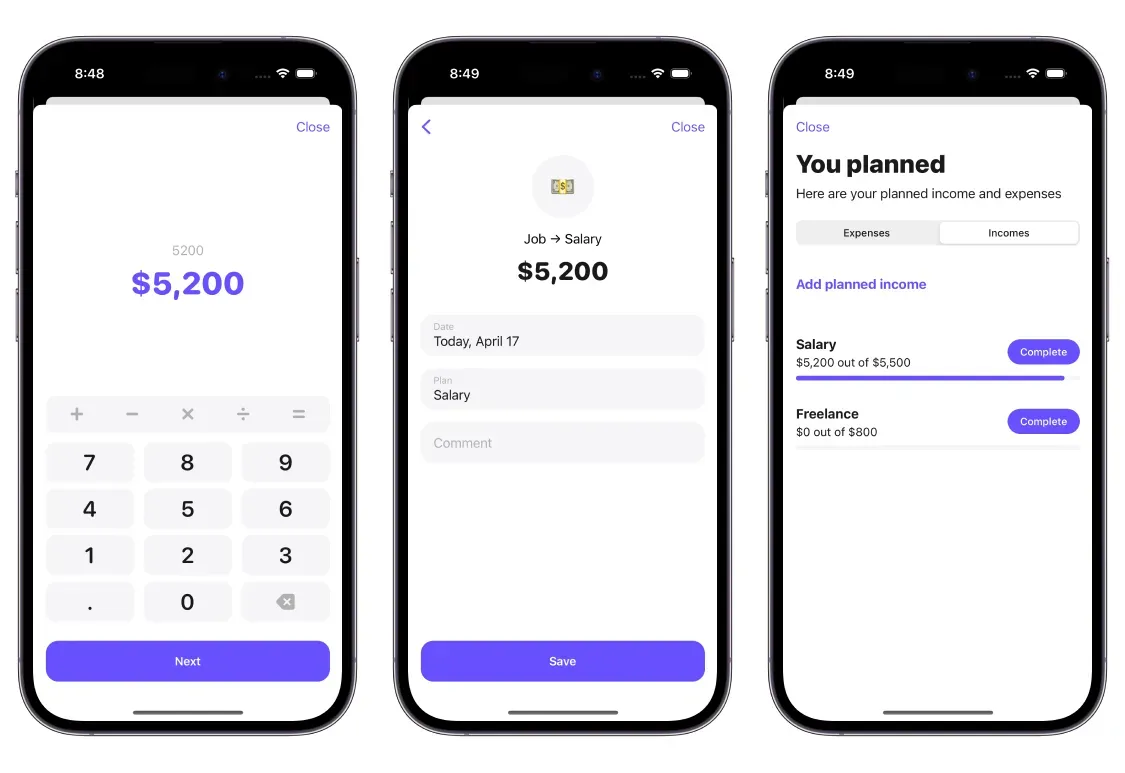

Adding an operation is very simple. We enter the amount, select the category, date, and indicate a plan if needed. These are the same plans that we created in the first stage — salary, taxi, dentist, etc.

At the planning stage, we create them as folders and now, as we manage the budget, fill them with real operations — expenses and receipts. After all operations have been added to the plan, it needs to be executed — that is, closed. I will give a few examples to make it clearer.

Examples:

- Instead of $5500, you received $5200 in salary because you were on vacation. Press “Complete” and now the budget will be recalculated based on the new amount, and it will be less. The new daily budget is $30.

- You spent $0 on the dentist instead of the planned $300. After completing the plan, $300 will be added to your free money sum, and it will all be recalculated automatically. The daily budget is $50 now.

- Do you want to save more money? No problem. Let’s change the amount from $630 to $830. Daily budget = $33.3.

There is another reason why the budget for the day may change. All the money you saved today also goes into the pool of free money. With the start of a new day, the budget will be recalculated, taking into account the remaining days. If you spend more, it will become less, as you are essentially reducing the pool of free money.

Budget check-up

Most apps only show you where your money’s going, but what about the beginning and middle of the month, when there’s still plenty of cash, and you’re tempted to spend it all? When it comes down to it, how much will be left at the end of the month? If you’re eyeing something expensive, can you afford it without having to live on bread crumbs until pay day? Will anything be put away for savings before the end of the month?

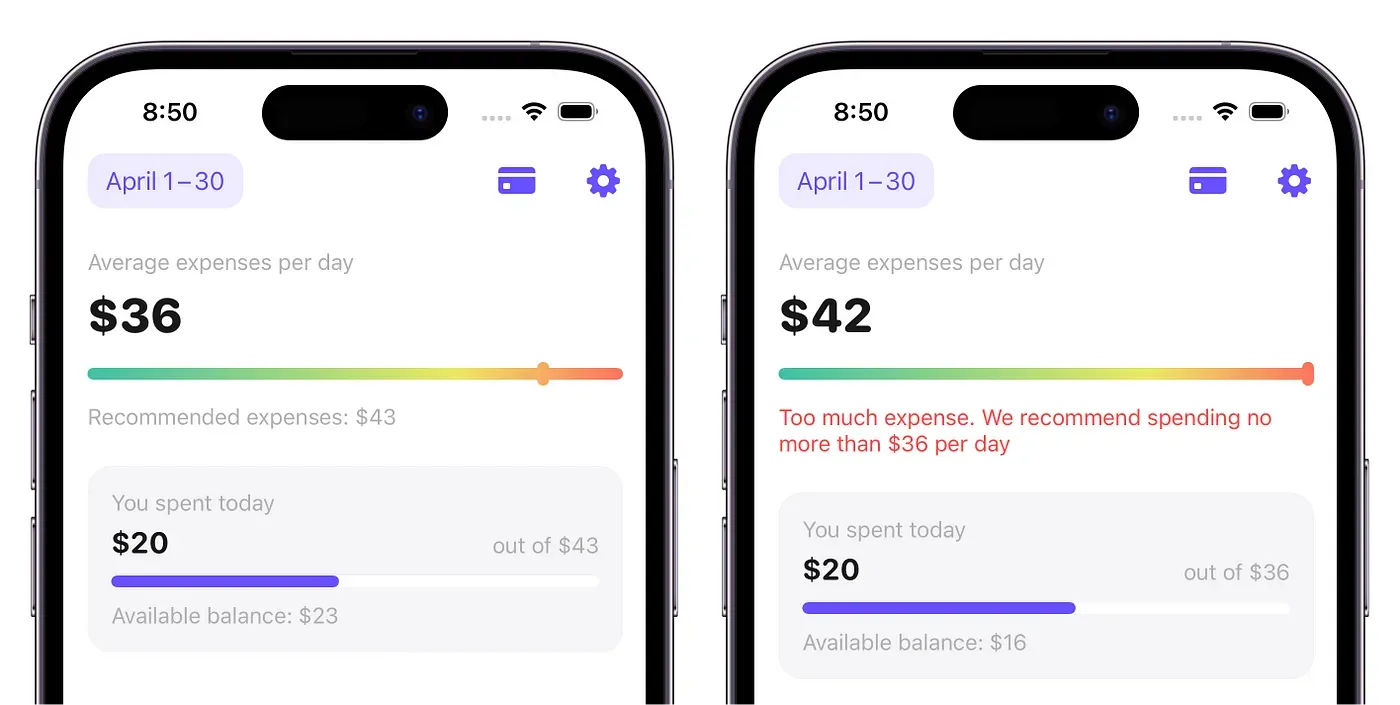

This is yet another problem that I was solving. We have plans and a daily budget, but we want to understand overall if the budget is deficit or not.

Here, I have added the most important health indicator of the budget — the average daily expenditure. This is simply the average value of your daily budget for the number of days since the beginning of the budget. The maximum limit is exactly your daily budget. Going beyond it means that you are regularly spending more than you can afford. By the end of period, there will be no money left.

Do you want to buy expensive sneakers? The easiest way to test your budget’s durability is to add a new plan and see what the program calculates.

Checking out expenses

The last, but no less important: analyze operations and find irrational or new categories. Expenses at the moment may seem small, but if analyzed over the entire period, a substantial amount can accumulate.

It may be the other way around: you think you are spending each day on something small, and in the end a large sum accumulates by the end of the month. In reality, it turns out that you spend more on weekends than during the whole month in this minor category. Our perception can deceive us.

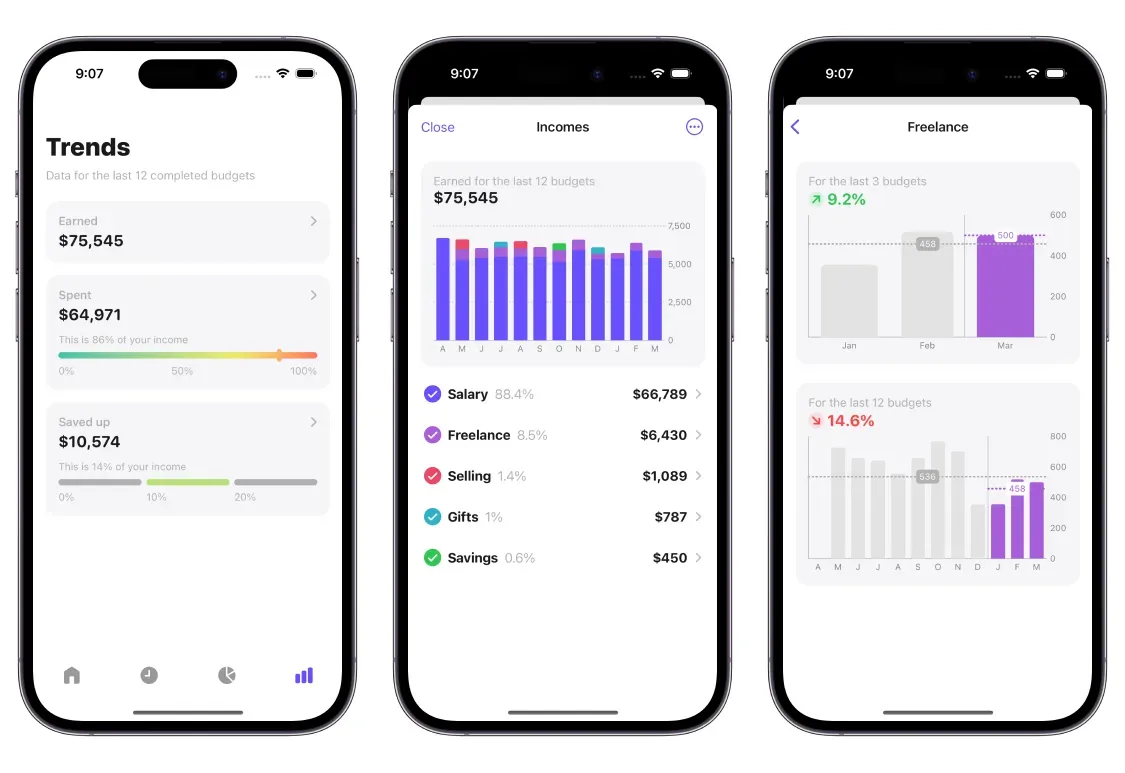

Until recently, you could only assess a specific budget, but in the latest version (iOS 16+), I added a new section called “Trends” which allows you to assess the overall picture within the last 12 budgets. You can also see how your habits change for each category and observe dynamics.

Instead of a conclusion

I hope you found the read interesting and that it gave you a bit of a nudge to get started on budgeting and taking more control of your finances (big shoutout to my pals who’ve hopped on the budget train!). Yep, budgeting ain’t easy. It takes serious commitment and motivation.

Share in the comments what strategies and tools you use to manage your budget, and which of my app’s features would be most useful for you. Can’t wait to hear your ideas!